The Central Laboratory Market: A Visionary Blueprint for 2024–2032

Redefining Precision, Scalability, and Strategic Decision-Making in Clinical Development

Executive Summary: The Era of Centralized Excellence

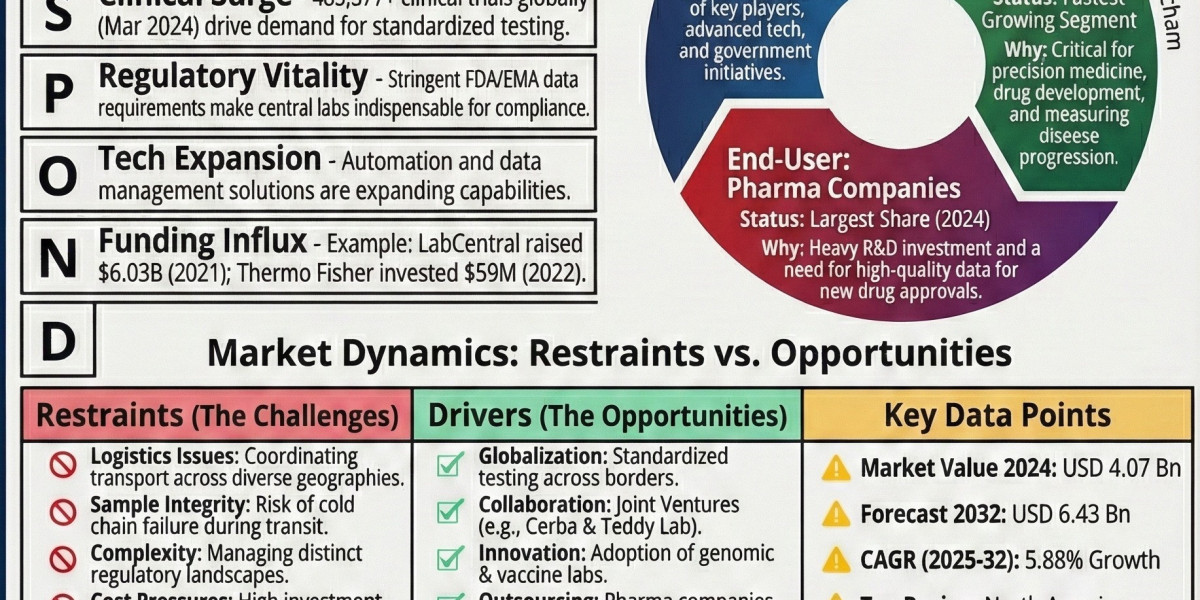

The global pharmaceutical landscape is undergoing a seismic shift. As therapeutic modalities evolve from broad-spectrum "blockbuster" drugs to highly targeted, patient-centric precision medicines, the infrastructure supporting their development must likewise transform. The Global Central Laboratory Market, valued at approximately USD 4.07 billion in 2024, is no longer a mere service provider; it has become the nerve center of the clinical trial ecosystem.

Projected to reach USD 6.43 billion by 2032 with a steady CAGR of 5.88%, this market represents the intersection of logistics, advanced molecular science, and big data. This report provides a 2,000-word deep dive into the strategic rewrite of the market's trajectory, focusing on clear vision, future business roles, and the pivot toward data-driven decision-making.

Access the Future of Market Strategy: [Download the Exclusive Sample Collection Kits Handbook & Data Summary Here] @ https://www.maximizemarketresearch.com/request-sample/148522/

1. Visionary Overview: Beyond the Laboratory Walls

The traditional view of a central laboratory—a facility that simply receives samples and returns results—is obsolete. The new vision for the central laboratory market is one of Integrated Intelligence.

In the next decade, central labs will function as "Scientific Command Centers." They will integrate real-world data (RWD), genomic profiling, and advanced logistics to provide a seamless flow of information from the patient’s bedside to the regulatory filing. This vision is built on three pillars:

Standardization: Ensuring that a blood sample in Mumbai is processed with the same precision and methodology as one in New York.

Specialization: Transitioning from routine safety testing to complex biomarker and genetic analysis.

Digitalization: Utilizing AI and cloud-based Laboratory Information Management Systems (LIMS) to offer sponsors real-time visibility into their trial’s progress.

2. Market Dynamics: The Engines of Growth

2.1 The Outsourcing Imperative

Pharmaceutical and biotechnology companies are increasingly divesting from internal laboratory infrastructure. By outsourcing to central labs, they convert fixed costs into variable costs, allowing for greater financial agility. This trend is particularly strong among small-to-mid-sized biotech firms that lack the capital to build global-scale labs but possess the innovative molecules that require them.

2.2 The Rise of Complex Biologics and Cell/Gene Therapy

The explosion of Cell and Gene Therapies (CGT) has created a demand for "Specialized Chemistry" and "Genetic Services." These therapies require ultra-complex monitoring, often necessitating cold-chain logistics that are integrated directly with the laboratory’s analytical capabilities. The central lab of the future is the only entity capable of managing the "Chain of Identity" and "Chain of Custody" required for these life-altering treatments.

2.3 Global Clinical Trial Expansion

Clinical trials are moving into emerging markets—Asia-Pacific, Latin America, and parts of Africa. Central laboratories provide the "Regulatory Bridge" needed to ensure that data collected in these regions meets the stringent standards of the FDA and EMA.

3. Segmental Intelligence: Where the Value Resides

3.1 Service Type: The Shift to Genetics and Biomarkers

While routine Safety Testing (hematology, urinalysis) remains the volume leader, the highest growth is seen in Genetic Services and Biomarker Testing.

Genetic Services: Anticipated to grow at a CAGR exceeding 7%, driven by the need for companion diagnostics.

Pathology & Histology: Essential for oncology trials, where central labs provide standardized "blinded" reviews of tissue samples to eliminate site-level bias.

3.2 End-User Profile: Pharma Leads, Biotech Accelerates

Pharmaceutical Companies: Hold the largest market share (approx. 45%), focusing on large-scale Phase III global trials.

Biotechnology Companies: The fastest-growing segment. Their reliance on central labs is total; they view the lab as a strategic partner rather than a vendor.

4. Regional Strategic Outlook

4.1 North America: The Innovation Hub

North America remains the dominant force, holding over 40% of the market. This is fueled by a massive R&D spend and a regulatory environment that favors advanced diagnostic integration. The focus here is on Next-Generation Sequencing (NGS) and AI-driven pathology.

4.2 Asia-Pacific: The Growth Frontier

The APAC region is the "engine room" of clinical trial expansion. With a CAGR nearing 9%, countries like India and China are not just "low-cost" destinations; they are becoming centers of excellence. The challenge and opportunity here lie in logistics—navigating diverse regulatory landscapes while maintaining sample integrity across vast distances.

5. The Role of Technology: The Digital Nervous System

To achieve the "New Version" of the central laboratory, technology must be the foundation.

Artificial Intelligence (AI): AI is being used to predict sample stability issues before they happen and to automate the interpretation of complex imaging and pathology slides.

Blockchain for Logistics: To ensure the integrity of the cold chain, blockchain is being explored to create an unalterable record of a sample's journey from the patient to the freezer.

Virtual/Hybrid Trials: Central labs are adapting to "decentralized" trials by offering home-collection kits and mobile phlebotomy services, bringing the lab to the patient.

6. Future Business Role: From Vendor to Strategic Partner

The business role of the central laboratory is shifting. In the "Old Version," the lab was a line item in a budget. In the "New Version," the lab is a Consultative Partner.

6.1 Early-Stage Involvement

Central labs are now being brought into the "Protocol Design" phase. By advising sponsors on which biomarkers are most viable or how to optimize sample collection at the site level, labs are reducing the "screen failure" rate of patients, saving sponsors millions of dollars.

6.2 Data Harmonization

The central lab is becoming a Data Aggregator. By providing unified data streams that can be plugged directly into a sponsor’s clinical trial management system (CTMS), the lab reduces the time required for "database lock," accelerating the path to market.

7. Proper Decision-Making: Strategic Recommendations for Stakeholders

For businesses to thrive in this evolving market, the following strategic decisions must be prioritized:

7.1 Investment in Specialized Capacity

Commodity testing is a race to the bottom on price. Decision-makers should pivot capital toward specialized services—genomics, rare disease assays, and cell-based assays—where margins are higher and competition is lower.

7.2 Strengthening the Logistics Backbone

The greatest risk to a central lab is "Sample Loss." Investing in proprietary logistics networks or deep-tier partnerships with specialized couriers (like World Courier or Marken) is not an option; it is a necessity for survival.

7.3 Embracing Sustainability

The "Green Lab" initiative is gaining traction. Future tenders will require labs to demonstrate reduced carbon footprints, sustainable waste management of biohazardous materials, and energy-efficient cold storage.

8. Navigating Challenges: The Roadblocks to Success

No market is without its hurdles. The central laboratory sector faces:

Regulatory Flux: Changing IVDR (In Vitro Diagnostic Regulation) in Europe and evolving FDA guidelines require constant compliance audits.

Talent Scarcity: There is a global shortage of molecular biologists and bioinformaticians. Companies must decide between "Buying" talent through high salaries or "Building" it through internal academies.

Geopolitical Tensions: Trade wars and regional conflicts can disrupt the global flow of biological samples, requiring labs to have "redundant" facilities in multiple geographic zones.

Elevate Your Competitive Intelligence: > [Click to Access the Complete Sample Collection Kits Strategy Handbook and Data Summary] https://www.maximizemarketresearch.com/market-report/central-laboratory-market/148522/

9. Conclusion: A Clear Path Forward

The Central Laboratory Market is at a crossroads. Those who continue to view it as a high-volume, low-margin testing business will eventually be marginalized. The "New Version" of this market belongs to the data-fluent, logistically-integrated, and scientifically-specialized players.

The vision for 2032 is a central laboratory that acts as a bridge between the laboratory bench and the patient’s life. By making the right strategic decisions today—investing in digital infrastructure, expanding specialized service portfolios, and embracing the role of a strategic consultant—market participants can ensure they don't just survive the evolution of clinical trials but lead it.

Key Takeaways for Business Leaders:

Vision: Move from "testing results" to "actionable insights."

Direction: Focus on the APAC region and the rise of Biotechnology.

Action: Audit your digital capabilities; if you aren't using AI and real-time tracking, you are already behind.

Decision: Prioritize "Value-Added Services" over "Routine Volume."